Imagine standing in your office corridor, reviewing a benefits package with a key employee who has a vital role in your company’s growth. You both want a safety net that supports their family if something happens, but you also want a policy that can serve strategic goals for your business. In that moment, a split-dollar life insurance arrangement can feel like the perfect bridge. It seeks to protect your people while also reinforcing your financial plan.

This option is more than an insurance contract. It can be a valuable agreement where both an employer and an employee share policy costs and benefits. For business owners, it’s an incentive tool that can boost loyalty and save money over time. For employees, it offers coverage with a lower direct cost. Let’s break down how split-dollar life insurance can help individuals, partnerships, and companies thrive.

Key Benefits

1. Shared Premium Costs

One major advantage of split-dollar life insurance is the shared approach to paying premiums. The employer covers a portion of the premium, and the employee (or sometimes another party) covers the rest. This helps manage expenses for both sides. By splitting the cost, a company can offer a valuable perk without bearing the entire burden.

2. Retention of Top Talent

In a competitive market, attracting and keeping high-performing employees can be challenging. A split-dollar arrangement can serve as part of an executive compensation package or a long-term incentive plan. The promise of life insurance coverage, combined with potential cash value growth, appeals to many key employees. This extra benefit often encourages them to stay, reducing turnover costs and helping with business continuity.

3. Tax-Efficient Strategy

When structured correctly, a split-dollar life insurance policy can offer tax benefits. For instance, the beneficiary may receive a death benefit that can be income-tax-free. The employer’s portion might also have certain tax-efficient features, though this varies with each arrangement. It’s wise to consult with a financial advisor or tax specialist to learn how the policy could fit your overall plan.

4. Cash Value Accumulation

Many split-dollar policies use permanent life insurance such as whole life or universal life. These products have a cash value component that grows over time. Depending on the agreement terms, the employee may access a portion of this cash value, providing liquidity for personal or business needs. This aspect can be especially appealing for those who want both life insurance protection and a long-term savings vehicle.

5. Estate Planning Possibilities

Split-dollar life insurance is often incorporated into estate planning strategies, especially for high-net-worth individuals. The arrangement can help transfer wealth to heirs or pay estate taxes. Some people also use a reverse split-dollar life insurance setup when they want the policy’s death benefit to flow more efficiently to designated beneficiaries. Integrating this policy into broader estate planning can be seamless when guided by legal and financial professionals.

How It Works

1. Basic Concept

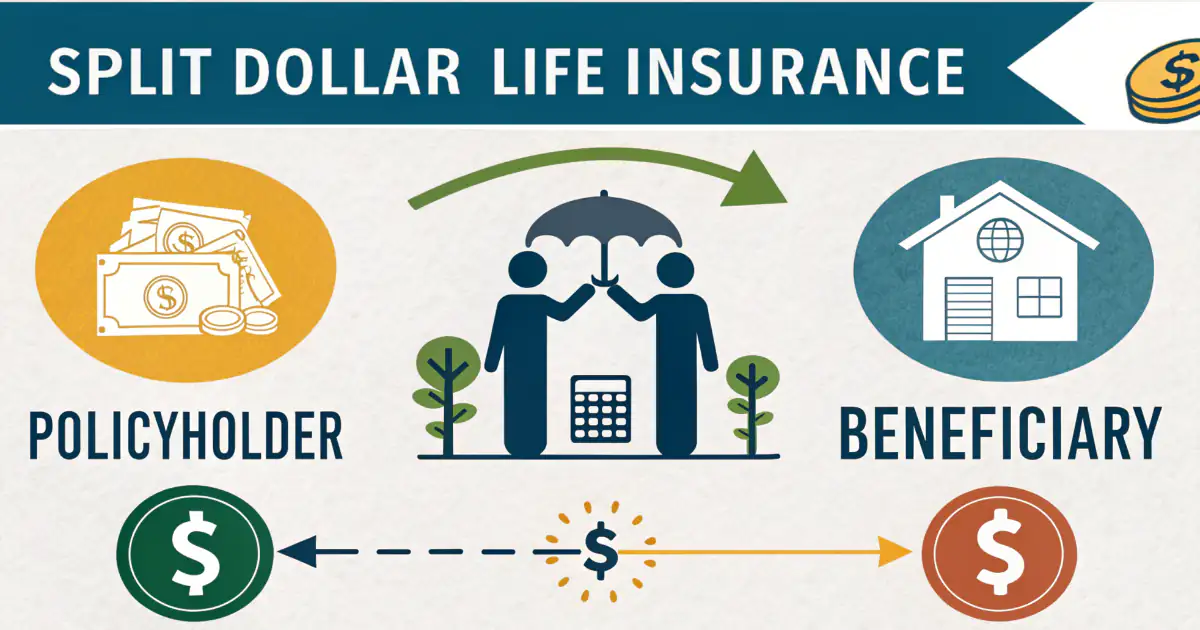

Under a split-dollar life insurance plan, two parties (often an employer and an employee) agree to share the rights and obligations of a life insurance policy. The employer might pay most or all of the premiums for a certain time. The employee may contribute a smaller amount or sometimes none at all. In return, they share the policy’s benefits and any cash value.

2. Formal Agreement

A legal document defines each party’s duties and what happens if the contract ends. This is critical because it details how proceeds are split if the policy is surrendered or if the covered person dies. It also explains repayment conditions if the employer expects reimbursement for premium advances. An endorsement method is one common approach, where the employer owns the policy and “endorses” a share of the death benefit to the employee or their beneficiary.

Another approach is a collateral assignment, where the employee owns the policy, but the employer has a security interest up to the amount they paid in. If you see references to a “split-dollar life insurance collateral assignment,” that’s exactly what it means: the employer’s contribution is secured by a lien on the policy’s value or benefit.

3. Funding and Repayment

Some arrangements require the employer to recover its premiums upon the insured’s death, after which the employee’s beneficiary receives the remaining death benefit. In other cases, the employer recovers its costs if the contract ends or the employee leaves. This structure ensures the employer is compensated for its share, while the employee enjoys protection and potential cash value buildup.

4. Utilizing a Calculator

Business owners and financial professionals often use a split dollar life insurance calculator to figure out optimal funding. This tool compares different structures, estimates future cash values, and calculates potential payout scenarios. Factoring in age, health status, and funding timelines helps both parties design a policy that aligns with their needs.

5. Possible Executive Compensation Setup

In split-dollar life insurance executive compensation, the arrangement might be a perk offered to high-level staff. It could include performance incentives and vested schedules that link policy benefits to tenure or achievements. In these cases, the agreement aligns personal goals with the company’s long-term interests. Once an executive fully vests, they might have more extensive access to the policy’s cash value or a guaranteed share of the death benefit.

Key Features & Coverage Options

1. Policy Type

Split-dollar life insurance often involves permanent policies, such as whole life or universal life. These policies have a cash value component that grows over time at either a fixed or variable rate. This gives the policy holder a chance to build equity while staying insured.

- Whole Life: Known for stable premiums, guaranteed cash value, and a level death benefit.

- Universal Life: Offers flexible premiums and potentially higher cash value growth, depending on market or interest rates.

2. Coverage Level

The face amount of the policy can vary. Some employers choose high coverage to ensure a meaningful death benefit for key employees and their families. Others pick more moderate coverage that still fulfills basic protection needs.

3. Cash Value Access

One of the main draws of permanent insurance is the ability to borrow against the cash value. If your arrangement permits it, the employee might access a portion of the accumulated cash. This can cover personal expenses or act as an emergency fund. The agreement should clearly outline any repayment conditions for policy loans, including interest rates and scheduling.

4. Ownership Arrangements

Ownership is a defining feature in split-dollar agreements. If the employer owns the policy, they can limit or endorse a portion of the benefits to the employee or their beneficiary. If the employee owns the policy, they grant the employer a collateral assignment. Each path has different tax and legal outcomes.

5. Payout Structure

Upon the insured’s death, the payout can be split between the employer and the employee’s beneficiaries. The employer typically recovers the premiums advanced, and the remaining death benefit goes to the designated beneficiaries. This split dollar life insurance payout can ensure the employer is compensated, while still granting a meaningful payout to the family.

6. Reverse Split-Dollar Setup

A reverse split dollar life insurance approach often aims to reduce gift taxes or shift more of the policy’s benefit to heirs. In this scenario, the employee (or trust) may pay a term cost for their share of the death benefit, while the employer holds an interest in the policy’s cash value. It’s a less common arrangement, but it can be helpful in certain estate planning situations.

Common Misconceptions

1. It’s Only for Large Corporations

Some believe that only big companies with huge benefits budgets can offer split-dollar plans. That’s not the case. While larger firms might find them easier to administer, smaller or midsize businesses can also benefit. A well-structured policy can serve as a key incentive, regardless of company size.

2. It’s Too Difficult to Understand

Split-dollar arrangements might seem complex at first, especially with terms like “collateral assignment” and “endorsement.” Yet most plans follow a simple guideline: the employer pays or advances part of the premium, and both parties share the policy benefits. A split-dollar life insurance example can clear up confusion by walking through actual figures. Working with an advisor who breaks down each element step by step makes the entire process more approachable.

3. It’s a Tax Dodge

Some individuals assume that split-dollar life insurance is a sneaky tax loophole. In reality, the IRS provides clear guidelines on how such arrangements should be taxed. Premium payments, interest, and benefit distribution all have distinct rules. When followed properly, a split-dollar plan can be part of a sound, lawful strategy.

4. It’s a One-Size-Fits-All Solution

Each split-dollar agreement can be unique. Factors like the participant’s age, health status, desired coverage, and business goals all shape the policy terms. The structure that works for one executive might not fit another. This is why most experts recommend customizing the contract to match specific objectives, rather than relying on a universal template.

5. It Lacks Liquidity

While it’s true that some policies lock in funds, the presence of cash value often provides avenues for borrowing. If designed with access in mind, a split-dollar policy can offer liquidity for personal or business needs. The key is ensuring the agreement outlines how and when you can draw from the cash value.

Expert Tips & Best Practices

1. Begin with Clear Goals

Define what you want to achieve before you commit to a split-dollar arrangement. Are you aiming to retain a top sales director for the long term? Do you want to provide life insurance coverage to a valued partner? Or are you seeking ways to manage your estate? Clear objectives help guide the structure of the agreement.

2. Consult a Professional

Split-dollar plans involve legal and tax considerations. A financial advisor or estate planning attorney can explain how federal and state rules apply to your plan. They can also detail how a split dollar life insurance estate planning setup might reduce estate taxes or pass wealth to heirs. Their expertise helps you avoid oversights and ensure the agreement fits your overall strategy.

3. Keep the Agreement Up to Date

A business evolves, and so do personal lives. Employees retire, switch companies, or face new financial demands. The same applies to business owners. Reviewing the split-dollar agreement every couple of years keeps it aligned with current goals. Adjusting coverage, premium contributions, or ownership can stop you from paying for a plan that no longer benefits everyone involved.

4. Run the Numbers

Leverage tools like a split-dollar life insurance calculator to estimate costs, future cash values, and potential death benefits. These projections help you confirm whether the arrangement makes sense for your situation. They also let you weigh the policy’s expected benefits against other investment or insurance options.

5. Document Everything

A written, legally binding contract is essential. Spell out who pays the premiums, who benefits from the death payout, and what happens if the employee leaves. Include how to handle policy loans or partial surrenders. Clarity reduces disputes and makes sure each side knows what to expect. Keep all paperwork in a secure place, and provide copies to relevant stakeholders.

6. Compare Pros and Cons

Many decision-makers evaluate alternatives like standard group life plans or supplemental benefits. While a split-dollar arrangement can offer significant perks—like cost-sharing and potential cash value it may also carry drawbacks, such as administrative fees or premium repayment obligations. Reviewing both split dollar life insurance pros and cons lets you decide if it’s the right fit.

7. Remain Compliant with Regulations

Authorities have guidelines on how split-dollar premiums and benefits are taxed. Depending on your structure, premium contributions might be seen as taxable income for the employee. The employer could owe taxes on certain policy gains. Keep track of changes in tax laws to avoid surprises down the road.

FAQs

1. What is a split-dollar life insurance?

A split-dollar life insurance refers to a contractual arrangement in which two parties, typically an employer and an employee, share the premiums and benefits of a life insurance policy. The employer may pay part or all of the premiums, and the arrangement details who owns the policy and how death benefits or cash value are divided.

2. How do you split life insurance money?

Splitting life insurance money depends on the agreement. Often, the employer recovers the amount of premiums it paid when the policy ends or when the insured individual dies. Any remaining death benefit goes to the employee’s beneficiary. The exact split is outlined in the contract and can vary based on ownership, repayment terms, and policy type.

3. Which is the cheapest life insurance plan?

The cheapest plan usually depends on individual factors like age, health, and coverage needs. Generally, term life insurance is the least expensive option for pure protection. But for split-dollar arrangements, most people opt for permanent policies like whole life or universal life because of their cash value and long-term benefits.

4. What is the most flexible life insurance policy?

Universal life insurance is often considered the most flexible because it allows you to adjust premium payments and coverage amounts within certain limits. This flexibility can be attractive in a split-dollar arrangement, as it offers room to adapt if personal or business circumstances change.

By following proven practices, reviewing real examples, and knowing the difference between various split-dollar structures, you can craft a policy that serves both your personal interests and your professional goals. When done well, split-dollar life insurance offers financial security for key employees while also benefiting the company that funds it.

Conclusion

A split-dollar life insurance arrangement can be a strategic solution for employers and employees. By sharing costs and shaping the policy for individual or business priorities, both parties can gain protection and potential financial growth. This setup can strengthen loyalty among your key people, offer a tax-friendly safety net, and even align with estate planning goals.

Before you commit, outline your goals. Make sure the agreement meets those aims, whether it’s retaining a top manager, helping heirs with estate taxes, or adding a safety net to an executive package. A qualified advisor can confirm that the structure suits your situation and remains compliant. With the right planning and consistent updates, a split-dollar policy can serve as a lasting benefit that protects both you and your business.